Do We Need Interest rate (KIBOR) or its Alternate to Run an Economy?

If Interest Is Eliminated from Pakistan’s Economy, How Will an Interest-Free Banking and Financial System Operate Without an Interest-Based Benchmark such as KIBOR? How Will Prices of Goods and Services Be Determined? How Will Monetary Control Be Exercised?

………………………………………………………………………………………..

اس آرٹیکل کے اردو ورژن کے لیے یہاں کلک کریں

VIDEO LINK of DISCUSSION – CLICK

……………………………………………………………………………………….

Dr. Muhammad Abubakar Siddique

Assistant professor, School of Islamic banking and Finance

International Islamic University Islamabad

………………………………………………………………………………………….

Brief Answer

If interest is eliminated from the economic system, there will be no need, in principle, for KIBOR or any new interest-based benchmark. Therefore, the very question of finding an “alternative” to KIBOR is conceptually misplaced. Why and how? This requires detailed explanation.

Detailed Answer

At first glance, this question appears to be a technical question, but in reality, it relates to the foundational philosophy of the Islamic financial system. Therefore, the answer is not merely that another numerical benchmark should be introduced in place of KIBOR. Rather, the real answer is that when the financial system moves away from an interest-based foundation and is restructured on Islamic principles, the entire concept of price determination changes.

In an interest-based system, a loan is treated as a means of earning profit. Therefore, such a system necessarily requires a rate through which the price of a loan is determined. KIBOR is part of this very interest-based logic. In an Islamic system, however, a loan is not a legitimate instrument for earning profit. Profit is earned through trade, ownership, risk-bearing, labour, rent, partnership, and real economic activity. Hence, in an Islamic system, the Shariah-based and rational need for an interest-based benchmark such as KIBOR no longer remains.

Confusion arises when one tries to imagine the practical operation of an Islamic financial system while still thinking within the framework of capitalism. This leads to doubts such as: “How will an Islamic financial institution operate without an interest rate?” One must first step out of that conceptual framework. Once interest is removed from the economy, the existing system will collapse under its own internal logic, because the entire capitalist financial structure largely stands on the crutch of guaranteed debt and interest. When that crutch is removed, the system will fall. Therefore, when the economy is reorganized on Islamic foundations, the importance of every interest-based component attached to the capitalist system will disappear.

The first point that must be clearly understood is that the Islamic financial system is not based on a single contract. In the interest-based system, almost every transaction ultimately returns to a loan and an increase over that loan. In contrast, Islamic financial transactions are conducted through different contracts, including sale, lease, partnership, muḍārabah, salam, istiṣnāʿ, agency, guarantee, and charitable contracts. Each contract has its own Shariah nature, economic logic, and method of price determination. Therefore, in an Islamic system, it is neither necessary, nor appropriate, nor consistent with the spirit of Islamic finance to determine the price of all financial transactions through one central rate.

The fundamental distinction of the Islamic system is that money itself is not treated as a tradable commodity. Money is a medium of exchange, a measure of value, and a means of payment. However, selling money for money with an increment is ribā under Shariah. By contrast, goods, assets, services, labour, skill, and business risk are legitimate sources of profit. This is why the Holy Qur’an states a clear principle:

“Allah has permitted trade and prohibited ribā.”

This verse does not merely state a legal ruling; rather, it lays down the foundation of an entire economic philosophy. Profit in sale is lawful because ownership of an asset is transferred, risk is borne, goods enter the market, demand and supply operate, and real economic activity is generated. In ribā, however, profit is taken merely against the passage of time, without the lender bearing trade risk or participating in any real asset. Therefore, in an Islamic system, profit will be linked not to a loan but to a genuine contract.

In light of this principle, when it is asked how prices will be determined without KIBOR, the answer is that the price of each contract will be determined according to the nature and requirements of that specific contract.

Four Basic Methods of Profit Determination

In the Islamic financial system, profit in every contract is determined according to its own Shariah and economic reality. Therefore, there is no room in the Islamic financial system for a single profit benchmark similar to KIBOR. Instead, different benchmarks and methods will exist according to the nature of different contracts. The remarkable feature of this system is that although these benchmarks are multiple, they are not complex like an interest rate. Rather, they are fully consistent with economic rationality.

Overall, profit determination in the Islamic financial system may be understood through the following four basic methods.

First Method: Profit Determination in Sales

The scope of sales in Islamic finance is very broad. It includes murābaḥah, musāwamah, salam, istiṣnāʿ, spot sales, deferred sales, instalment sales, and other permissible forms of sale. In all these cases, the basic principle of profit determination is the same: in a sale, profit may be fixed either as a lump-sum amount or as a specific percentage of the price of the commodity.

For example, on a commodity priced at Rs. 100,000, a profit of Rs. 10,000 may be fixed, or a profit of 10 percent may be charged, which would amount to the same Rs. 10,000. This is permissible because the owner of the commodity bears the risk of ownership and therefore has the right to earn profit from it. Shariah has not fixed a specific ceiling for profit in a sale. However, there is certainly an ethical limitation: profit should not be earned by exploiting the hardship or compulsion of another party. At this point, the role of the state becomes important.

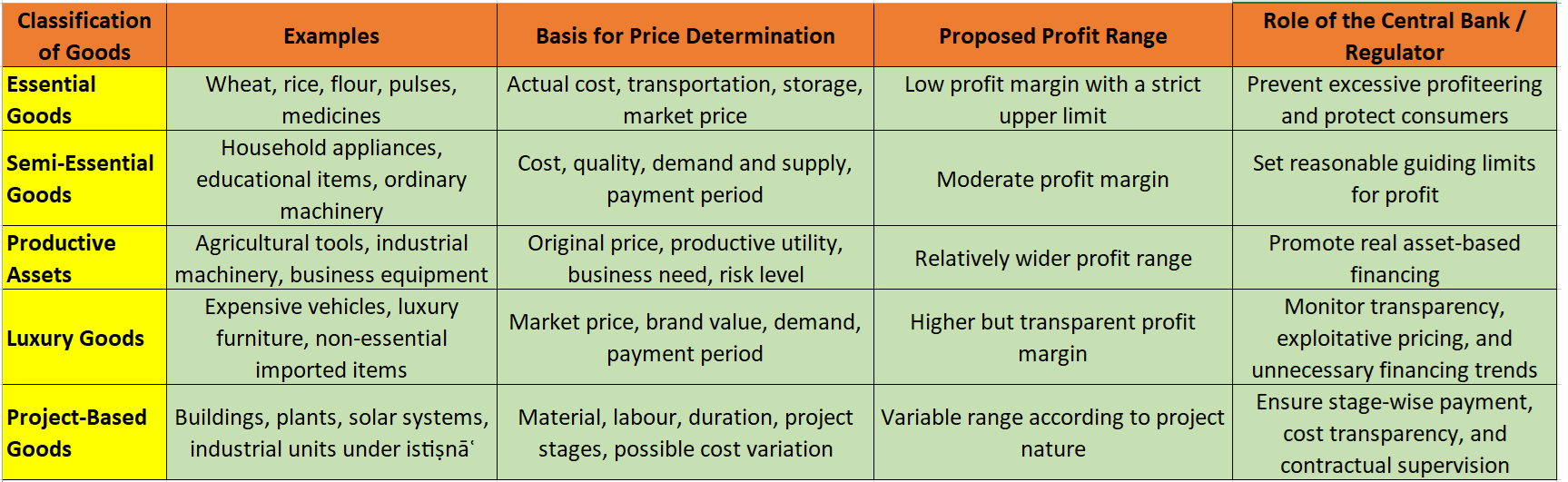

In sale-based financing by financial and banking institutions, the central bank may play an important regulatory role. It may classify commodities and prescribe upper and lower indicative profit margins for each category.

Table 1: Regulatory Framework for profit Determination in Sale-Based Financing

The basic purpose of this table would be to link sale-based Islamic banking financing with real commodities, actual cost, market conditions, payment period, ownership risk, and lawful commercial profit, instead of KIBOR. In this system, the central bank would not determine an interest rate. Rather, it would regulate commodity classification, indicative upper and lower profit margins, transparent pricing, consumer protection, and prevention of unjust profiteering. In this way, sale-based financing would remain connected with real trade and the asset-based economy, instead of becoming an interest-based loan.

Second Method: Profit Determination in Ijārah

In ijārah, the return on usufruct is called rent. In this contract, the financial institution becomes the owner of an asset and grants the customer the right to use that asset. In return for this use, the customer pays rent. Rent may also be determined on the principle of sale, meaning that a specific amount may be fixed, such as Rs. 10,000, or rent may be determined as a certain percentage of the value of the asset.

The rent will be determined with reference to the usufruct of the asset, prevailing market rent, duration of use, value of the asset, responsibility for repair and maintenance, depreciation, ownership risk, and nature of use. For example, rent cannot be the same for a house, vehicle, machinery, factory, office, agricultural equipment, or industrial plant. The rent of each asset will be determined according to its usufruct and market conditions.

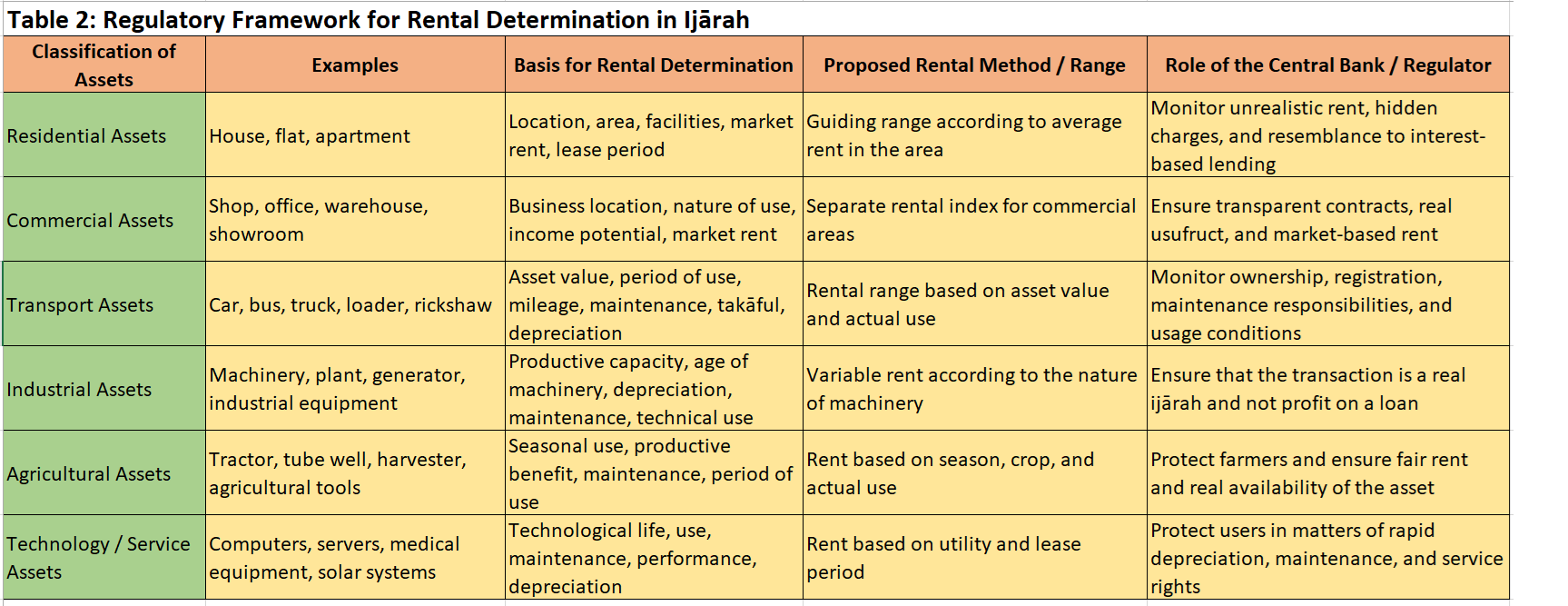

As in sales, assets may be classified in ijārah, and rent may be determined according to the nature of each category. The central bank or regulatory authority may issue guidelines for different types of assets so that ijārah is not used as a disguised interest-based loan. Instead, real ownership, usufruct, and rent must genuinely exist.

For this purpose, a method may be developed for classifying assets and determining rents accordingly, similar to the classification of goods in sale-based financing. A proposed table may be placed here:

The basic objective of this framework would be to ensure that rent in ijārah is determined on the basis of the real usufruct of the asset, prevailing market rent, period of use, depreciation, repair and maintenance, ownership risk, and nature of use, rather than KIBOR or any interest-based benchmark. The central bank or regulatory authority may develop a rent-guidance index for different assets. However, this would not be an interest rate; rather, it would be a regulatory mechanism to keep ijārah connected with real ownership, real usufruct, and lawful rent. Thus, ijārah would operate not as a substitute for an interest-based loan but as an independent Shariah contract.

Third Method: Profit Determination in Partnership (Video Lecture)

In partnership, the financial institution is not a lender; rather, it becomes a partner in the business or asset. In this structure, the concept of price does not appear in the form of an interest rate. Instead, a profit-sharing ratio is agreed upon.

- In partnership-based contracts, profit is not determined in the same way as in sale or ijārah.

- In partnership, profit is fixed in term of percentage (%) of total unknown unearned future profit.

- No specific amount (minor or major) can be fixed in favor of any partner.

- Profit cannot be fixed in term of percentage of invested capital.

Here, the central bank (SBP) may play a regulatory role by establishing a principle for partnership-based investment. For example, it may stipulate that the profit share of an Islamic bank should correspond to its share in capital, because the Islamic bank will generally be a non-working partner.

In this case, the problematic two-tier profit structure often found in running mushārakah arrangements would also be avoided.

The central bank may also prescribe rules regarding transparency, accounting, responsibility for loss, rights of partners, use of capital, profit distribution, and disclosure of risks in partnership transactions. However, the core principle will remain that the financial institution must participate in the actual business outcome, rather than merely giving a loan and receiving a guaranteed increase.

Fourth Method: Profit Determination in Muḍārabah

In muḍārabah, one party provides capital, while the other party provides labour, expertise, and management. In this contract as well, there is no room for KIBOR or a predetermined interest-based rate. Profit in muḍārabah is determined through a ratio of actual profit-sharing. For example, it may be agreed that 60 percent of the profit will go to the capital provider and 40 percent to the muḍārib, or any other ratio may be mutually agreed upon. Therefore, muḍārabah also does not require KIBOR.

It is not valid in muḍārabah to stipulate that the capital provider must receive a specific fixed amount or a predetermined annual return in all circumstances. If such a condition is imposed, the essence of muḍārabah will be destroyed, and the transaction will become close to a loan with profit. In a valid muḍārabah, profit must be linked to the actual business outcome. If profit is earned, it will be distributed according to the agreed ratio. If loss occurs, the capital loss will be borne by the capital provider, provided that the muḍārib has not committed negligence, misconduct, breach of trust, or violation of the agreement.

The central bank may also formulate rules for muḍārabah. It may prescribe upper and lower indicative limits regarding how much of the total profit may be retained by the muḍārib and how much may go to the rabb al-māl when profit is realized. These limits would not be considered an interest rate, because they would apply only to actual realized profit and not to a guaranteed return on capital.

The Role of the Central Bank

It is incorrect to assume that the abolition of KIBOR would weaken the role of the central bank. In reality, the role of the central bank in an Islamic system would become more meaningful, although its nature would change. Instead of setting an interest rate, the central bank would focus on the regulation of Islamic financial contracts, supervisory standards, transparency requirements, financial stability, money supply, market supervision, the soundness of financial institutions, and protection of the public interest.

The central bank would continue to regulate the economy in an Islamic system, but not through the interest rate. Rather, it would regulate through Shariah-compliant contracts, real assets, market supervision, and financial justice.

Is the State Bank’s Role Satisfactory?

The role of the State Bank of Pakistan in promoting Islamic banking is clearly encouraging, particularly after the Federal Shariat Court’s judgment of April 2022 and the 26th Constitutional Amendment. The State Bank has not treated the elimination of interest as a merely theoretical or political slogan; rather, it has translated this objective into a formal policy direction through SBP Vision 2028 and the strategic plan for 2024–2028. Its recent measures, including the guidelines issued in June 2024 for the conversion of conventional banks into Islamic banks, the facilitation of conventional branch conversion into Islamic branches from October 2024, the strengthening of the Sharīʿah Governance Framework effective from 1 January 2025, and the implementation of AAOIFI Sharīʿah Standard No. 47 in January 2025, show that the central bank is moving from general commitment to practical regulatory action. These steps indicate a serious institutional effort to transform banking operations, governance, products, staff capacity, customer awareness, and Sharīʿah compliance mechanisms.

The numerical evidence also supports this conclusion. By December 2025, Islamic banking assets in Pakistan had reached Rs. 14,467 billion, while deposits had increased to Rs. 11,037 billion. The share of Islamic banking in the overall banking industry rose to 22.9 percent in assets, 27.8 percent in deposits, and 38.1 percent in financing. The branch network also expanded to 7,562 Islamic banking branches. These figures demonstrate that Islamic banking is no longer a marginal or symbolic segment of Pakistan’s financial sector; it has become a major and growing component of the banking industry. Therefore, it may be concluded that the State Bank of Pakistan’s role is not only encouraging but also strategically significant. However, the success of this transformation will depend on sustained regulatory pressure, stronger Sharīʿah governance, genuine product development, professional training, and effective coordination among regulators, banks, Sharīʿah scholars, economists, and policymakers.

Public Finance and Ṣukūk

In the existing system, governments usually borrow through treasury bills and interest-bearing bonds. In an Islamic system, these instruments may be replaced by ṣukūk. Ṣukūk are not merely certificates of debt. Rather, they must be linked with real assets, projects, ijārah, partnership, muḍārabah, or another acceptable Shariah structure. In ṣukūk, investors do not receive interest. Instead, they receive a share from the rent of an asset, the profit of a project, or lawful business income.

For example, the government may issue ṣukūk based on a road, building, energy project, port, airport, government buildings, or other real assets. Investors would hold a Shariah-recognized right in relation to the asset or its returns. If the ṣukūk are structured on ijārah, the return will be in the form of rent. If they are structured on partnership, the return will be linked to the actual performance of the project. In this way, the government will be able to raise financial resources, while investment will also be mobilized without interest-based borrowing.

May Allah Almighty grant our ruling authorities abundant ability to establish the system of the Beloved Holy Prophet ﷺ, and may He enable us to play a positive role that is accepted in His court.

Āmīn, bi-jāh al-Nabī al-Karīm al-Amīn ﷺ.

Good & very informative