Pakistan’s Debt Story: Past, Present, and the Hope for the Future

(Path to an Interest-Free Economy and National Recovery)

۔۔۔۔۔۔۔۔۔۔۔۔۔۔۔۔۔۔۔۔۔۔۔۔۔۔۔۔۔۔۔۔۔۔۔۔۔۔۔۔۔۔۔۔۔۔۔۔۔۔

For Urdu Version – Click Here

…………………..

Dr. Muhammad Abubakar Siddique

School of Islamic banking and Finance

International Islamic University Islamabad

………………………………………………………………………………………….

June 13, 2026

……………………………………………………………………………………….

Why Are We Suffering from This Disease?

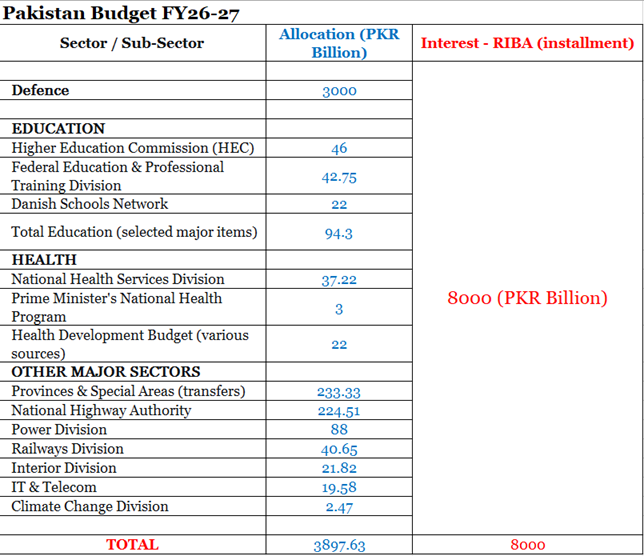

When a patriotic Pakistani looks at the country’s recent budget 2026—totaling 18,771 billion rupees (18.77 trillion rupees)—and realizes that out of this, 8,000 billion rupees are earmarked solely for interest payments on debt while the principal debt amount remains untouched, and further sees that the entire defense budget is only 3,000 billion rupees, their heart bleeds.

When most state revenue goes toward debt servicing, little remains for education, health, water, agriculture, industry, technology, employment, or public welfare. The government borrows for development, for running the budget, and to repay old loans—creating a vicious cycle that repeatedly drags Pakistan to external financial institutions. The recklessness and failures of one specific class of this generation are being borne not only by the whole society but will also haunt the next generation. Therefore, we must begin treatment now. First, understand the disease and its root cause so that diagnosis leads to a possible cure. The real disease is the interest-based economic system, and the lethal bacterium is riba (interest) itself.

The Core Problem: Riba, Not Just Debt

The fundamental flaw of Pakistan’s economic system is that it detaches money from the real economy and entitles it to guaranteed returns. The government borrows on interest to cover fiscal deficits. Banks park funds in secure government papers to earn risk-free profits, leaving little incentive to lend to private businesses. As a result, supply of loanable funds for the private sector becomes limited, forcing farmers, industrialists, and exporters to pay exorbitant interest rates. Meanwhile, the public is crushed under inflation, heavy taxes, and unaffordable utility bills. Instead of being directed toward farms, factories, export industries, skills, and productivity, national wealth is consumed by debt servicing. This is why Pakistan has repeatedly sought interest-based financial bailouts from the IMF and others—but the root cause remains untreated.

The Quranic Warning Against Riba

When a Muslim society structures its entire economy on interest without real production, labor, risk, or partnership, then economic anxiety, restlessness, injustice, debt pressure, and collective weakness descend from the heavens.

The entire annual budget for the nation’s well-being — education, health, roads, electricity, railways, provincial development, farmers, laborers, and the poor’s bread — is just 3,897 billion rupees. Yet this same nation is forced to pay 8,000 billion rupees in interest (riba) alone (see following table). Think about it: a nation burns more than double of what it spends on its own survival and human dignity — just to feed the monster of interest. Why? The answer is painfully simple, yet unbearable to accept: your war against Allah and His Messenger ﷺ has turned back on you. This is not an economic failure — it is an open declaration of war from Allah Himself. The Qur’an warns: “If you do not give up riba, then be prepared for war from Allah and His Messenger” (Al-Baqarah 2:279). Today, that very war is devouring your homes, your schools, your hospitals, your roads, and your children’s future. Riba has taken the entire nation hostage. Until you repent from this filthy, cursed system, every new project, every prayer, every tear — will continue to be sacrificed at the altar of interest.

This is no surprise, for Allah says: “And whoever turns away from My remembrance—indeed, he will have a depressed life, and We will gather him on the Day of Resurrection blind” (Quran 20:124-125). Nations that turn away from Allah’s commands are deprived of vision (basirah) despite having intellect. Shaitan makes them so irrational that they consider increasing the interest rate as the cure—while the disease worsens. Yet Allah’s mercy is that if the Ummah returns to the straight path, His blessings are restored. The question is: When will we repent from this ongoing war with Allah and abolish riba completely?

How Much Public Debt Does Pakistan Owe?

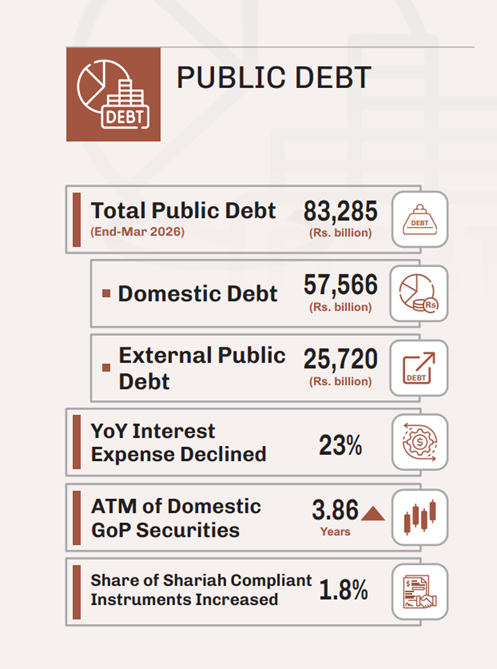

Pakistan’s total direct domestic and external debt stands at approximately 83.28 trillion rupees. Domestic debt accounts for ~57 trillion rupees (borrowed from banks, national savings schemes, and financial institutions), while external debt is ~26 trillion rupees. Total public debt is estimated between 70–83% of GDP.

Has Pakistan’s Debt Actually Decreased?

No. The reality is not that the country’s debt burden has reduced, but rather that its rate of increase has moderated. As of March 2026, public debt continues to stand at elevated levels. However, during the last nine months, debt grew by only 3.4 percent, compared to 6.7 percent recorded in the same period a year earlier. In other words, the ailment is still spreading—only at a slower pace.

Several factors explain this deceleration: (1) reduction in the policy rate has lowered the cost of new borrowings; (2) decreased reliance on expensive short-term Treasury bills has eased pressure on debt accumulation; (3) a shift from short-term floating-rate instruments to long-term fixed-rate government bonds has reduced vulnerability to sudden interest rate hikes; (4) buyback of expensive old bonds and their replacement with new, lower-interest bonds have helped contain costs; (5) and a modest increase in the share of Shariah-compliant sukuk has been observed—though this remains very small relative to total public debt.

A more systematic and rapid transition to an interest-free financial structure is urgently needed. If lowering interest rates has brought measurable relief, one can only imagine the transformative impact that eliminating interest altogether could have on Pakistan’s economy.

Government Assets vs. Debt

Pakistan possesses vast and valuable assets, including land, buildings, highways, ports, airports, energy infrastructure, and state-owned enterprises. Yet, despite their significance, there exists no complete, transparent, reliable, or unified national asset registry. Consequently, the true market value of total government assets remains unknown—a major administrative failure that undermines effective policymaking.

Adding to the concern, several state-owned entities—including Pakistan International Airlines (PIA), Pakistan Steel Mills, Pakistan Railways, and the power distribution companies (DISCOs)—have turned into long-term liabilities due to persistent operational losses. With proper management, professional oversight, and productive discipline, these institutions could be transformed into income-generating assets. Instead, weak governance and chronic political interference have crippled their potential.

In an interest-free economic framework, these assets should not be hastily sold off for temporary cash relief. Rather, they ought to be revitalised into sustainable, revenue-generating assets through genuine Islamic financing instruments such as sukuk, ijarah, musharakah, public-private partnerships, awqaf-based development models, and productive leasing arrangements. Under such an approach, ownership remains with the state while generating steady streams of rent, services, production, employment, and broader public benefit. Without a complete and transparent record of what the state owns, Pakistan cannot effectively leverage its own wealth to reduce debt or generate revenue. You cannot manage or monetize what you do not know.

When Did Pakistan Fall into the Debt Trap?

Pakistan did not fall into debt trap suddenly. The history spans decades: 1958 saw the first approach to IMF for balance of payments support; the 1970s brought nationalization policies, oil price shocks, and rising fiscal pressures; the 1980s added the Afghan war, defense needs, external aid, and growing debt reliance; the 1990s witnessed political instability, weak reforms, and external payment pressures; from 1998 onward, economic sanctions increased external financing needs; the 2000s offered some debt relief, but the opportunity was not fully used to strengthen exports, tax base, or productivity; the 2010s saw large infrastructure projects, energy costs, import pressures, and external debt; and from 2018 onward, rupee depreciation, energy costs, interest payments, fiscal deficits, and a deeper debt trap have persisted.

In every era, debt was largely used for consumption, imports, current expenditures, political priorities, and repaying old debt—not for building productive capacity. New debt became a tool to repay old debt. Debt stopped being a solution and became part of the problem.

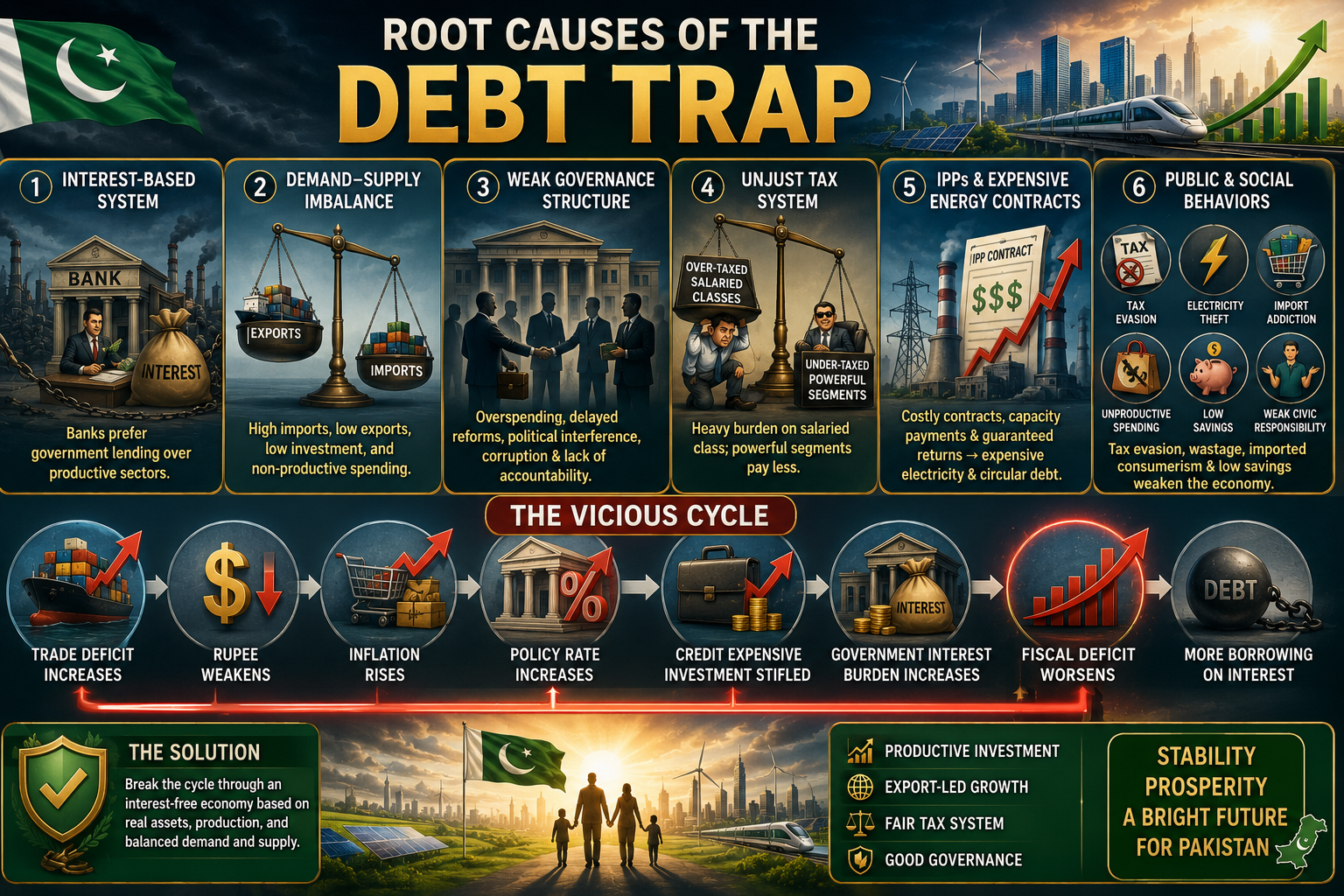

Root Causes of the Debt Trap

First, the interest-based system guarantees returns to capital while weakening its link to production, risk, labor, and business outcomes. Banks prefer lending to the government at secure margins rather than to industry, agriculture, SMEs, or exporters. The real economy weakens while the debt economy strengthens.

Second, there is a persistent aggregate demand and supply imbalance. Pakistan’s private consumption has been very high but largely dependent on imported goods—fuel, food, machinery, and raw materials—rather than local production. Investment has remained low, and much of it went into non-productive or low-productive sectors. Government spending often exceeded revenues and was directed toward non-productive priorities. Exports have remained narrow, while imports consistently exceeded exports, creating a trade deficit financed by external debt. The interest system deepened this imbalance.

Third, weak governance structure: governments spent beyond means, delayed tax reforms, failed to fully tax powerful elites, allowed political interference in state enterprises, and sought solutions in new debt. Allegations of kickbacks, commissions, money laundering, weak accountability, and a culture of privileges eroded trust between citizens and the state.

Fourth, an unjust tax system: salaried classes are easy targets because their income is documented. Lower and middle-income groups are crushed under direct taxes, electricity bills, inflation, and indirect taxes—while undocumented businesses, real estate, large agricultural income, wholesale-retail networks, and influential segments contribute proportionally less. When citizens see sacrifice demanded only from them, tax compliance weakens.

Fifth, IPPs and expensive energy contracts: Independent Power Producers were introduced to increase generation and competition, but weak policies, opaque contracts, government guarantees, dollar-indexed payments, costly imported fuel, lack of competitive bidding, capacity payments, political patronage, powerful interests, and allegations of corruption made them a permanent burden. Payments are due regardless of whether electricity is produced or consumed. The result is expensive electricity, circular debt, higher industrial costs, weaker exports, and more borrowing.

Sixth, public and social behaviors: tax theft, electricity theft, undocumented business, imported consumerism, disinterest in local products, unproductive expenditure, and low savings also contribute to national weakness. If rulers do not act with integrity and citizens do not accept responsibility, the economy cannot strengthen. Both the state and society need reform.

In summary, the interest system made this imbalance dangerous. Trade deficits increased dollar demand, the rupee weakened, and inflation rose. To control inflation, the central bank raised the policy rate—making private sector credit expensive and stifling productive investment—while simultaneously increasing the government’s interest burden. Banks earned billions without effort. The fiscal deficit worsened. To cover it, the government borrowed more on interest. This is the vicious cycle that brought Pakistan to the IMF’s door. An interest-free economy has the potential to break this cycle because investment and consumption are tied to real assets and production, not artificial demand created by interest.

What Should Pakistan Do?

The Government

The government must pursue the complete elimination of riba as the core strategic objective. This requires closing the door to all new interest-based loans and progressively reducing reliance on conventional Treasury bills and Pakistan Investment Bonds. Instead, the government should finance its needs through genuine Islamic financing instruments, including sukuk, ijarah, musharakah, mudarabah, salam, istisna, and project-based Islamic finance. Simultaneously, existing interest-based debt must be transformed through a phased and negotiated restructuring process—seeking forgiveness, reduction, rescheduling, or Shariah-compliant conversion of the interest component from lenders and international financial institutions.

A complete national asset registry must be established. Every government-owned asset—land, buildings, highways, ports, airports, energy assets, state-owned enterprises, and commercial assets—must be recorded and their fair market value determined. Instead of fire sales for short-term cash, these assets should be converted into sustainable, income-generating assets through Shariah-compliant models such as sukuk, ijarah, musharakah, waqf, and public-private partnerships, while retaining public ownership and ensuring long-term revenue, employment, and public benefit.

The government must also balance aggregate demand and supply by reducing unnecessary import consumption, conspicuous expenditure, and non-productive government spending while simultaneously boosting agriculture, industry, technology, skills, food processing, value-added textiles, the halal industry, minerals, SMEs, and exports. Redirecting demand from imports to local production and strengthening domestic supply chains will ensure that economic growth does not repeatedly trigger balance of payments crises.

On energy, the government must conduct independent and transparent reviews of all IPP contracts and condition capacity payments on actual availability, performance, and efficiency rather than mere presence on the grid. Dollar-indexed payments must be revisited, and reliance on expensive imported fuel reduced. All future energy projects should be based on competitive bidding, local resources, renewables, demand planning, and Shariah-compliant financing. Energy should support production and exports—not debt.

The Ruling Elite

To restore public trust, the ruling elite must lead by action, not speeches. This requires reducing unnecessary privileges, protocols, official amenities, foreign visits, political hiring, and unproductive expenditures. Transparent asset declarations must be mandatory for all senior officials, elected representatives, bureaucrats, and powerful elites. Above all, the law must apply equally to the powerful and the weak. Trust will only return when ordinary citizens see the elite sacrificing alongside them—not living above the law.

The Elite Class (Large Business, Real Estate, Agriculture, Wholesale-Retail, Industrialists)

The elite class must accept national responsibility and join the tax net. This means documenting businesses, paying workers’ full rights, enhancing local value addition, and focusing on exports. It is time to shift from rent-seeking to productive roles. If the state provides land, electricity, security, and policy support, then the elite must contribute genuinely to the national economy—through taxes, investment, job creation, and ethical business practices. A country cannot prosper when the wealthiest contribute the least.

The General Public

The general public must also play its part. Citizens must actively reduce tax theft, electricity theft, undocumented business, imported consumerism, unnecessary expenditure, and disinterest in local products. Instead, they should embrace simplicity, savings, local production, halal business, tax payment, zakat, sadaqat, waqf, qard hasan (benevolent loans), skills, education, and an entrepreneurial mindset. The public is willing to step forward, but they need truthful leadership. When rulers demonstrate integrity and trustworthiness, the people will sacrifice.

Establish a Riba-Free Economic Recovery Commission

Finally, Pakistan must establish a “Riba-Free Economic Recovery Commission” comprising Shariah scholars, economists, the Ministry of Finance, the State Bank, SECP, legal experts, bankers, industrialists, provincial representatives, the export sector, energy experts, and public representatives. This commission must produce a time-bound roadmap for ending new interest-based loans, Shariah-compliant conversion of existing debt, a national asset registry, authentic sukuk, IPP reforms, tax justice, discipline in government expenditures, an export mission, demand-supply balance, and connecting the private sector to productive Islamic finance.

The Real Path to Freedom from the IMF

The real path to freedom from the IMF is simple: Pakistan must stop eating by taking loans and start earning by producing. The very purpose of a riba-free economy is to lift money out of the vicious cycle of interest, consumption, and debt, and instead connect it to assets, trade, production, employment, justice, self-reliance, and economic sovereignty. When private consumption shifts toward local production, when investment flows into genuine industry and agriculture, when government spending becomes productive, when exports rise and the burden of imports falls—then, and only then, will Pakistan gain the real foundation to escape the debt trap. This path is religiously sound, economically viable, nationally necessary, and the only sustainable road to Pakistan’s lasting recovery.

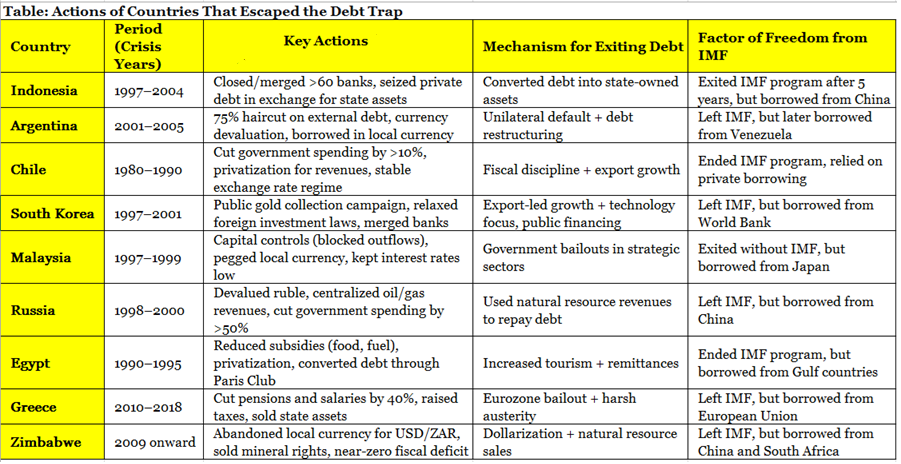

The path described above—a riba-free economy—has not been attempted by any of the countries in the table below. Nevertheless, their experiences offer general evidence that escaping IMF dependence is possible through structural reforms.

The following table summarizes countries that, in the recent past or in history, became trapped in a debt crisis and later made successful or semi-successful attempts to exit their dependence on the International Monetary Fund (IMF). In this table, the “Period” refers to the time when these countries initiated harsh reforms to escape debt, and by the end of that period, they had exited the IMF program (although they continued to borrow from other sources). This table is based on data and case studies from the World Bank, the IMF, and academic literature.

May Allah Almighty grant us guidance to the Straight Path. May He bestow upon us abundant ability to understand the schemes of Satan, to avoid them, and to break them, and may He keep us under His protection.

O Gracious Lord! May we witness with our own eyes the abolition of the interest-based (riba) system and the sunrise of the Islamic economic system in the blessed country of Pakistan.

Āmīn, bi-jāh al-Nabī al-Karīm al-Amīn ﷺ.

………………………….

Citation:

Siddique, M. A. (2026, June 13).Pakistan’s Debt Story: Past, Present, and the Hope for the Future (Path to an Interest-Free Economy and National Recovery). IslamicFina. (https://islamicfina.com/pakistans-debt-story-past-present-and-the-hope-for-the-future/)

Good observations by Respected Sir